The Analysis: Lovys

From renters to pets, 🏡🐾 Lovys is reshaping insurance. But is it truly groundbreaking?

It’s time to have a look at Lovys, which has launched its Equity Crowdfunding Campaign at Crowdcube platform. Expect a 8-minute read, and please note this is not financial advice.

Founding Team 👨🏼💻

João Cardoso De Jesus, Co-Founder & Co-CEO: With a background in economics and advanced studies at Wharton and London Business School, João founded VisionX and TaCerto.com before Lovys. His career includes leadership in B2B2C insurance platforms, M&A at Morgan Stanley, and investment roles at Forum Partners, emphasizing innovation in finance and insurance.

Elise Moutarlier, Co-Founder & former COO at Lovys: A Paris-Sorbonne graduate in international relations, Elise co-founded Lovys, France’s first all-digital insurance platform, scaling operations to 40k clients and designing its initial insurance products. Since early 2024, Elise has shifted her focus to Combak.co, a second-hand and refurbished goods comparator, leaving Lovys after 5 transformative years.

Funding 💰

Investors

Heartcore, NewAlpha, Raise Ventures, Maif Avenir, Portugal Ventures and Bpifrance: €17 million (2021)

MAIF Avenir, Portugal Ventures and Bpifrance: €3.3 million (2019)

Startup Sesame: Undisclosed amount (2018)

Partech and Techstars: €106k (2017)

Other investors include: Plug And Play, Raise Ventures, Adevinta, MS & AD and Fin TLV.

Total Funding Amount: €20.4 million

Last Valuation: €24.7 million

Business Model 🧩

Value Proposition

Lovys simplifies insurance with a fully digital, all-in-one platform offering flexible, subscription-based coverage for home, car, health, and more. Acting as an intermediary, it designs user-friendly products and leverages AI and automation for seamless claims handling and customer support. Lovys addresses the need for transparency and flexibility, aligning with modern expectations.

Customers

B2C:

Young Adults & Millennials: They seek flexible, transparent insurance with digital-first interfaces, addressing pain points like jargon-heavy processes and policy confusion.

Urban Dwellers: They value hassle-free subscriptions for essentials like home, car, and smartphone insurance, aligning with their need for simplicity and control.

B2B2C: Strategic Partners: Lovys collaborates with corporations to embed seamless, innovative insurance solutions into partner ecosystems, enhancing customer retention.

Offering

B2C Products:

Home Insurance: Flexible policies for renters, homeowners, and landlords, tailored to specific needs.

Car Insurance: Covers civil liability, personal injury, and legal defense for drivers.

Bike Insurance: Provides protection against theft, damage, and liability for cyclists.

Pet Insurance: Includes vet visits, medical costs, and surgery without deductibles.

Smartphone Insurance: Protects against accidental damage, water damage, and theft.

Borrower’s Insurance: Ensures loan repayments in case of illness, accident, or death.

Health Insurance: Covers medical costs, including consultations, treatments, and hospital stays.

B2B2C Services:

Partner Integration Program: Businesses can embed Lovys insurance products directly into their offerings.

Integration Tools: APIs, tracked links, and custom buttons allow seamless embedding into partner platforms.

Partner Management Tools: Dedicated dashboards for monitoring sales and client activity.

Monetization

B2C: Earns commissions on insurance contracts.

B2B2C: Integrates its digital insurance platform into third-party ecosystems, offering embedded insurance solutions to partners.

Operations

Lovys services are currently available in France, Spain and Portugal.

Growth 📊

Credentials 🏅

Elected one of the best 100 startups to invest in 2020 by Challenges Newspaper.

Works with major insurance players like Allianz and Generalli.

Currently has +50 B2B2C partnerships live, including with Younited Credit and Floa.

Market Size 🌍

The European insurtech market is poised for significant growth, with estimates projecting an increase from €43.21 billion in 2024 to €286.47 billion by 2032, reflecting a CAGR of 26.67%. This expansion is fueled by technological advancements such as AI, blockchain, IoT, and cloud computing, which streamline risk assessment, claims processing, and operational efficiency. These innovations enable insurance providers to offer customer-centric solutions that meet the evolving expectations of digital-savvy consumers.

Key drivers include increasing investor interest and strategic collaborations that accelerate innovation and market penetration. Additionally, regulatory support and rising consumer demand for transparent, efficient insurance products are creating a favorable ecosystem for insurtech firms. Cloud adoption further enhances cost-efficiency and scalability, allowing companies to focus on core growth areas while maintaining agility in service delivery.

In conclusion, the European insurtech industry represents a dynamic and growing segment, with strong potential for further expansion as technology integration deepens and customer expectations continue to drive innovation. This growth trajectory highlights the increasing relevance of digital-first insurance models in meeting the needs of modern consumers.

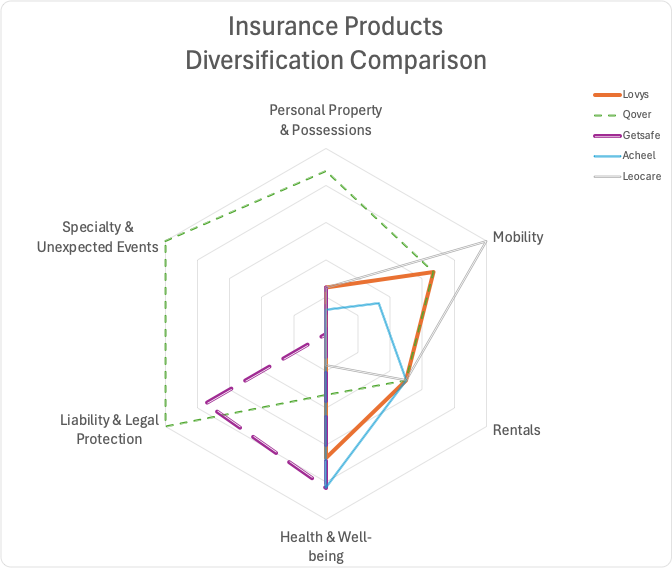

Competition 🤼♂️

Qover

Based in Belgium, Qover provides embedded insurance solutions for digital businesses, integrating APIs for offerings like gig economy protections, mobility coverage, and employee benefits. It operates in 32 countries in Europe, supporting brands like Deliveroo and Revolut with over 2 million users.

Getsafe

Headquartered in Germany, Getsafe focuses on digital-first, app-based insurance. It offers modular personal lines like liability and renters’ insurance, primarily targeting young customers. Getsafe serves over 500k policies in its home-market, Germany, and also Austria, France and the UK.

Acheel

Acheel, based in France, is a 100% digital insurer specializing in health, home, and pet coverage with straightforward, customizable policies. Licensed in France, and recently authorized to operate in Portugal and Spain, so far it has gained 500k customers.

Leocare

French-based Leocare provides multi-line mobile insurance for car, home, and smartphone users, focusing on flexible subscriptions and eco-friendly practices. Licensed in France and Spain, it boasts over 300k users, appealing to a tech-savvy and environmentally conscious audience.

Competitiveness 💪🏼

Lovys’ competitiveness in the insurtech space reveals both strengths and challenges when compared to its peers. While its offerings are broad, covering mobility, health, and well-being insurance, it doesn’t lead in any specific segment. Mobility insurance, where it performs relatively well, tends to be less lucrative than other lines, limiting its edge. In contrast, its Health & Well-being products are notable, but competitors like Getsafe and Acheel deliver more comprehensive solutions in this area, with offerings such as pet insurance and bill protection.

One area where Lovys lags is its client base and geographic reach. It has the fewest customers among the competitors, limiting its scale and ability to compete with Qover’s 2 million users or Leocare’s 300,000. In terms of geographic coverage, Qover sets a high bar with operations in 32 countries, while Lovys has yet to achieve similar breadth. Additionally, Lovys lacks standout features like Qover’s cyber protection or Getsafe’s investment services, which cater to niche needs and attract diverse audiences.

Lovys’ direct-to-consumer (B2C) model offers some flexibility compared to Qover’s exclusively B2B2C focus, but it doesn’t leverage a unique selling proposition to differentiate itself in the crowded insurtech market. Its position in the market is further tested by Acheel’s diversified clientele (B2B, B2C, and B2B2C) and innovative extras like home alarm systems, which bring added value to customers.

In conclusion, Lovys competes effectively with a broad range of products and a focus on both B2C and B2B2C markets. However, its lack of specialization in high-demand segments like liability or unique features seen in competitors limits its differentiation. Despite its smaller customer base and geographic reach compared to leaders like Qover, Lovys shows promise in areas like Health & Well-being and Mobility insurance, which can serve as a springboard for further growth. By refining its offerings and exploring innovative or niche segments, Lovys could better position itself to compete against more diversified and established players.

Roadmap 🧭

Product Development: Create innovative insurance solutions for evolving customer needs.

AI Integration: Enhance customer experience using personalized, AI-driven tools and processes.

Marketing Expansion: Promote “Insurance 2.0” through targeted, impactful marketing campaigns.

Portfolio Growth: Acquire customer portfolios to expand market presence and scale.

Digital Transformation: Digitize operations for efficiency and seamless customer interactions.

What we like 👍

Experienced Leadership: João Cardoso, co-founder and CEO, brings deep expertise in the insurance sector.

Strong Partnerships: Over 50 B2B2C partners provide stability and growth opportunities.

Revenue Growth: Revenue doubled between 2022 and 2023, indicating strong business momentum.

Growing Industry: Operates in an industry with a projected CAGR of 26.67% in coming years.

Trusted Backers: Collaborates with major insurance players like Allianz and Generali.

What we don’t like 👎

Equity Concerns: Low funding valuation suggests founders may retain limited equity, raising commitment questions.

User Growth Stagnation: Added only 5k users from 2021 to 2024, down from 15k between 2020-2021.

Competitive Pressure: Competes with larger insurtechs like Qover, which have significantly more clients and stronger product or market differentiation.

Limited Differentiation: Struggles to stand out due to similarities in products and lack of a unique market approach.